Your dog just ate a sock. Not a metaphorical sock — an actual tube of cotton that’s now sitting somewhere between his stomach and small intestine. The vet says surgery will run about $3,000. Maybe more if there are complications. You’re standing at the front desk doing mental math you never expected to do on a Tuesday afternoon.

This is the moment most people suddenly care about pet insurance. And it’s the worst possible moment to start shopping.

The smarter move is understanding what pet insurance costs before the sock incident — and that cost depends heavily on where you live. A dog owner in Arkansas might pay half what someone in New York pays for nearly identical coverage.

So what does the average pet insurance cost by state actually look like, and is the premium worth it once you stack it against what vets charge in your area?

That’s exactly what we’re breaking down here, using data from Insurify, the North American Pet Health Insurance Association (NAPHIA), and veterinary cost research from the American Veterinary Medical Association (AVMA).

What the Average American Pays Right Now

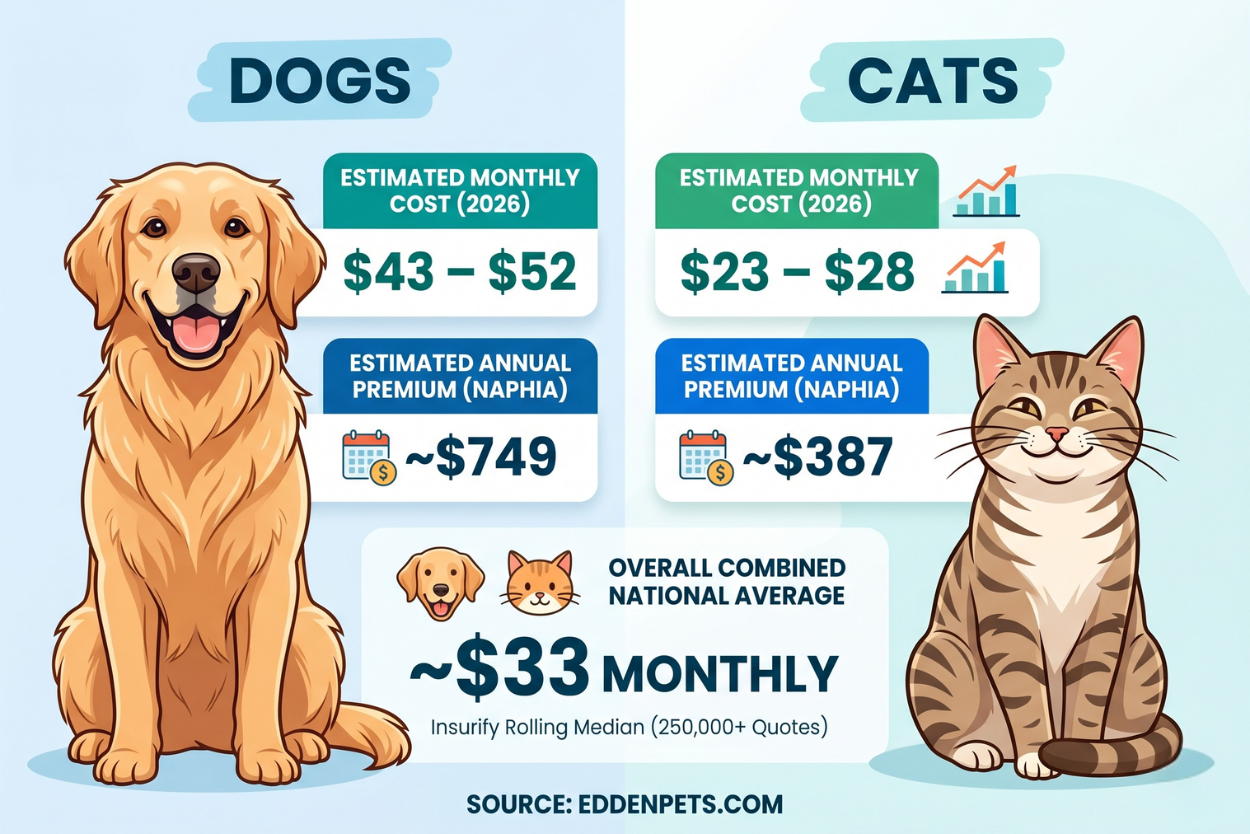

Before we get into state-level differences, here’s the national baseline. The average monthly cost of pet insurance in 2026 is roughly $43–$52 for dogs and $23–$28 for cats, depending on which dataset you use.

Insurify’s rolling median across 250,000+ quotes puts the combined national average at about $33 per month. NAPHIA’s latest annual figures — which lean toward accident-and-illness plans specifically — report average annual premiums of around $749 for dogs and $387 for cats.

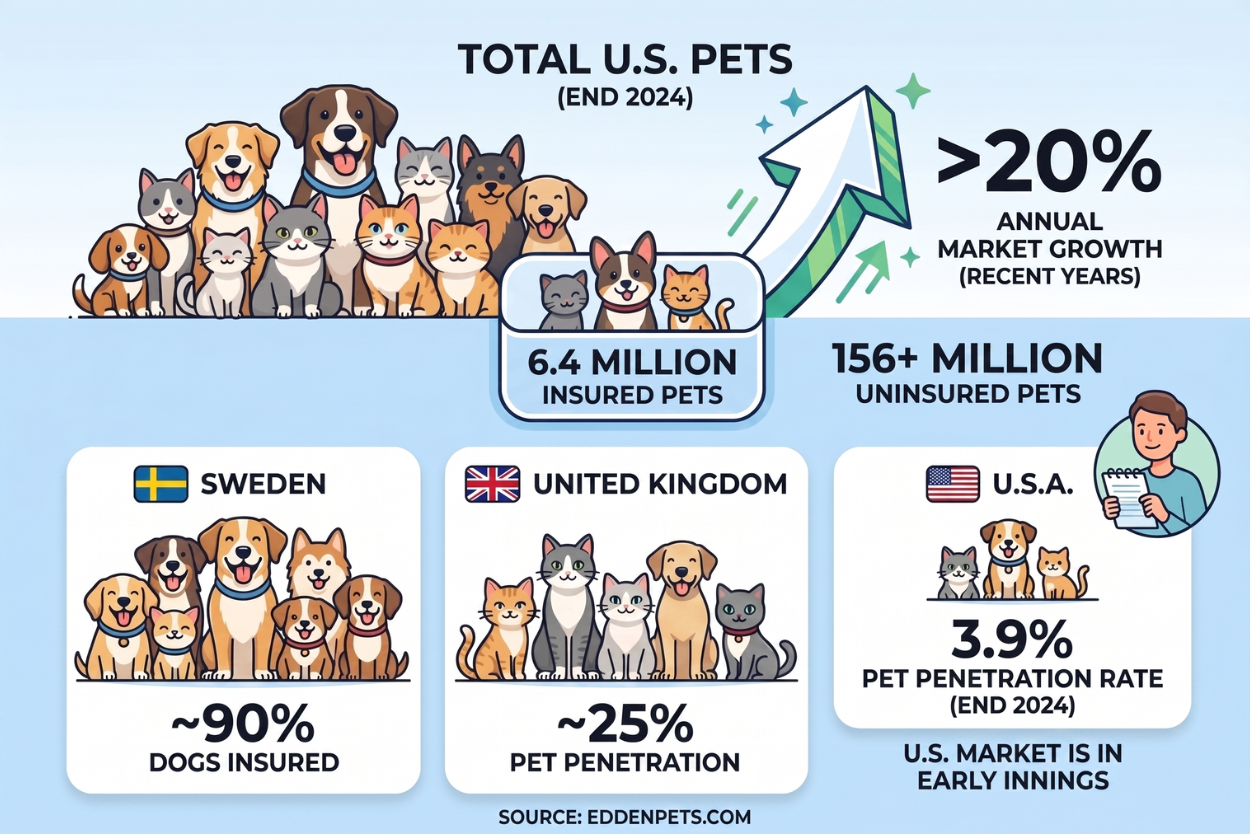

Those numbers have been climbing. The U.S. pet insurance market pulled in over $4.7 billion in gross written premium in 2024, up more than 20% from the prior year. That’s a market that has more than doubled since 2020.

Yet for all that growth, fewer than 4% of American pets carry any insurance at all. Compare that to Sweden, where roughly 90% of dogs are insured, or the United Kingdom, where penetration sits around 25%. The U.S. is still in the early innings.

A “typical” policy in these averages covers accidents and illnesses at an 80% reimbursement rate with a $250–$500 annual deductible. That’s the plan most people buy, and it’s the benchmark you should keep in mind as you read the state-by-state numbers below.

Pet Insurance Cost by State: Who Pays the Most and Least

Here’s where it gets interesting — and where the national average stops being very useful. Pet insurance premiums vary by state because vet costs vary by state, and insurers price their products accordingly.

The table below shows estimated average monthly pet insurance premiums for dogs and cats in all 50 states and Washington, D.C. These figures are compiled from Insurify quote data, NAPHIA industry reports, and Consumer Affairs research.

All averages assume a standard accident-and-illness policy. Your actual quote will vary based on breed, age, deductible, and ZIP code.

Cost tiers are based on each state’s position relative to the national average: Low (10%+ below), Mid (within ±10%), High (10%+ above). Source data from Insurify (rolling medians through March 2026), NAPHIA 2025 State of the Industry Report, and MoneyGeek analysis. Figures are rounded estimates; your actual premium will differ.

Now, what patterns jump out from this data?

The Most Expensive States

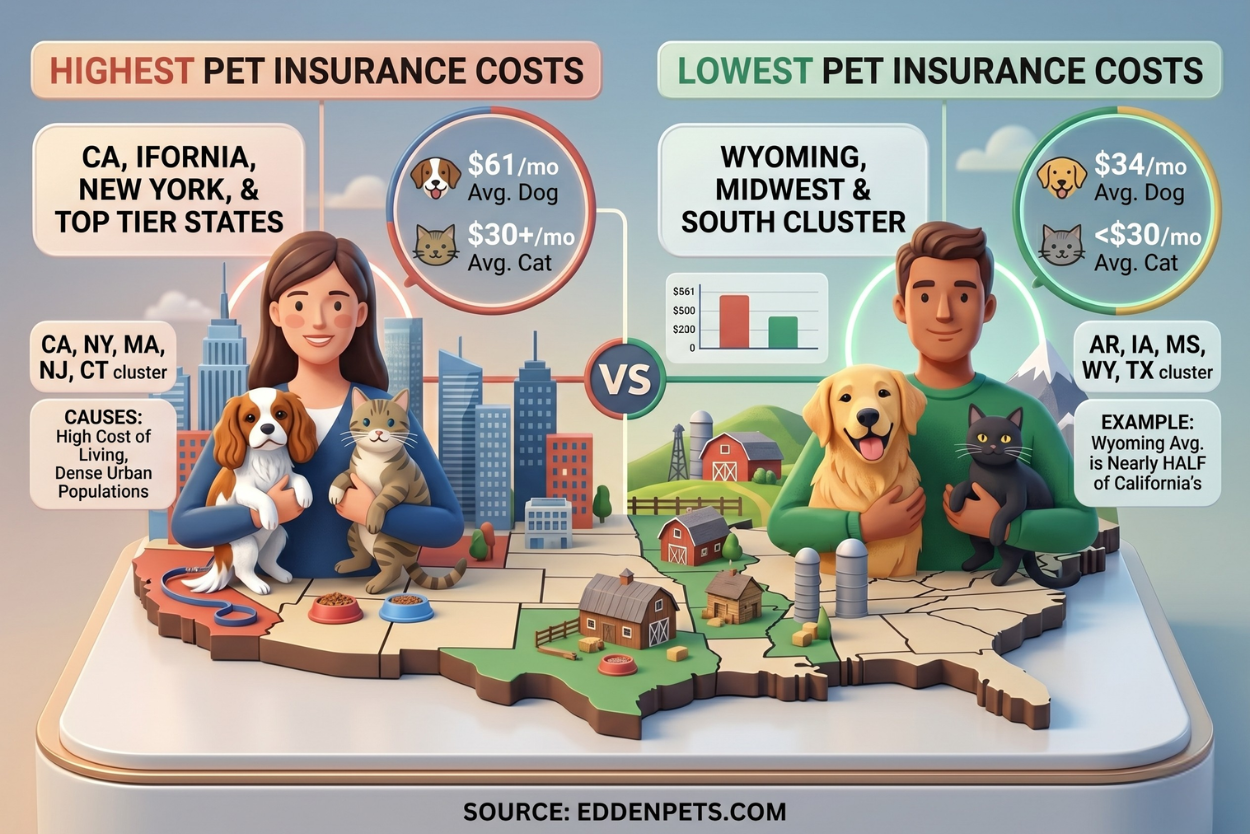

States with high costs of living and dense urban populations consistently top the list. California leads the pack, with average monthly dog insurance premiums around $61. New York is right behind at roughly $61 as well. Massachusetts, New Jersey, and Connecticut round out the top tier, all hovering at $50 or above for dogs and $30+ for cats.

Why? It mostly comes down to what vets charge. A veterinary practice in Manhattan or downtown LA has higher rent, higher staff salaries, and access to more expensive diagnostic equipment.

Those costs flow directly into insurance pricing. If your local vet charges more for an ACL repair, your insurer adjusts your premium upward to account for the likelihood of paying that larger claim.

The Cheapest States

The five cheapest states for pet insurance cluster in the Midwest and the South. Arkansas consistently sits well below the national average, and states like Iowa, Mississippi, Wyoming, and Texas offer some of the lowest premiums in the country. Dog insurance in Wyoming averages roughly $34 per month — nearly half what Californians pay.

Rural states tend to have lower vet costs across the board. Fewer specialty practices, lower overhead, and less demand for after-hours emergency clinics all contribute to smaller claims for insurers, which translates to smaller premiums for you.

The Surprising Middle

Then there are the states that don’t quite fit the pattern. Florida, for example, has a relatively high cost of living but moderate pet insurance rates, partly because the state has a competitive insurance market with a lot of provider options.

Colorado and Washington run higher than you might expect for their size, driven by urban hubs like Denver and Seattle where vet costs rival coastal cities. Keep in mind: your premium is tied more closely to your ZIP code than your state boundary. Two towns 50 miles apart can produce meaningfully different quotes.

What’s Actually Driving the Price Differences?

State averages are useful, but they can also be misleading if you don’t understand the levers behind them. Five factors account for most of the variation you’ll see from one quote to the next.

1. Regional vet costs are the biggest factor

The Bureau of Labor Statistics Consumer Price Index for veterinary services rose nearly 8% annually in 2023 and 2024, well above general inflation. But those increases haven’t been evenly distributed.

Urban areas with specialist vet practices — places where you can get an MRI for your dog at 2 a.m. — charge significantly more than rural general-practice clinics. Insurers know this, and they adjust by ZIP code.

2. Your pet’s breed matters enormously

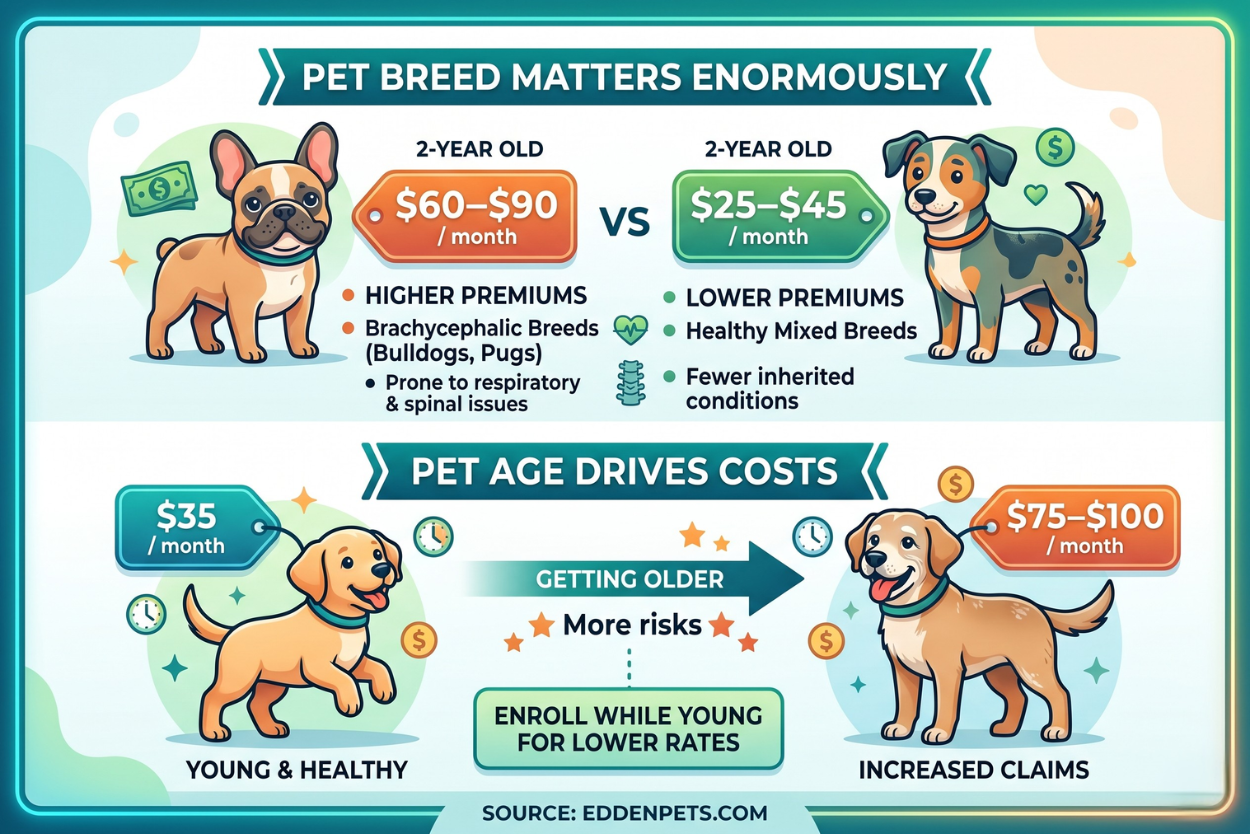

A 2-year-old French Bulldog will cost dramatically more to insure than a 2-year-old mixed breed, even in the same city. Brachycephalic breeds (Bulldogs, Pugs, Boston Terriers) are prone to respiratory issues and spinal problems.

Large breeds like Great Danes and Bernese Mountain Dogs carry elevated risks for heart conditions, joint issues, and certain cancers. Monthly premiums for a French Bulldog can run $60–$90, while a healthy mixed breed might come in at $25–$45.

3. Age is the second-biggest driver after breed

Insuring a 1-year-old Labrador might cost $35 per month. That same Lab at age 8? You’re looking at $75–$100. Premiums climb steadily as pets age because older animals file more claims. This is the single strongest argument for enrolling your pet while they’re young.

4. The coverage level you choose changes the math

Raising your deductible from $250 to $500 can cut your monthly premium by 10–20%. Dropping your reimbursement rate from 90% to 70% lowers it further. These aren’t just abstract numbers — they’re the trade-off between what you pay monthly and what you’ll owe out of pocket when a claim hits.

5. State-level insurance regulation plays a smaller but real role

Some states require insurers to submit rate filings for review, which can moderate pricing. Others have enacted pet insurance-specific consumer protection laws that standardize what policies must disclose, indirectly affecting how plans are priced and marketed.

Cost vs. Value: Does Pet Insurance Actually Pay Off?

This is the question everyone eventually asks, and the honest answer is: it depends on the pet.

Pet insurance isn’t an investment. It’s a risk-transfer tool. You’re paying a known monthly cost to avoid an unknown — and potentially devastating — future expense. Whether that trade-off makes financial sense depends on what kind of pet you have, where you live, and how much veterinary risk you’re comfortable absorbing out of pocket.

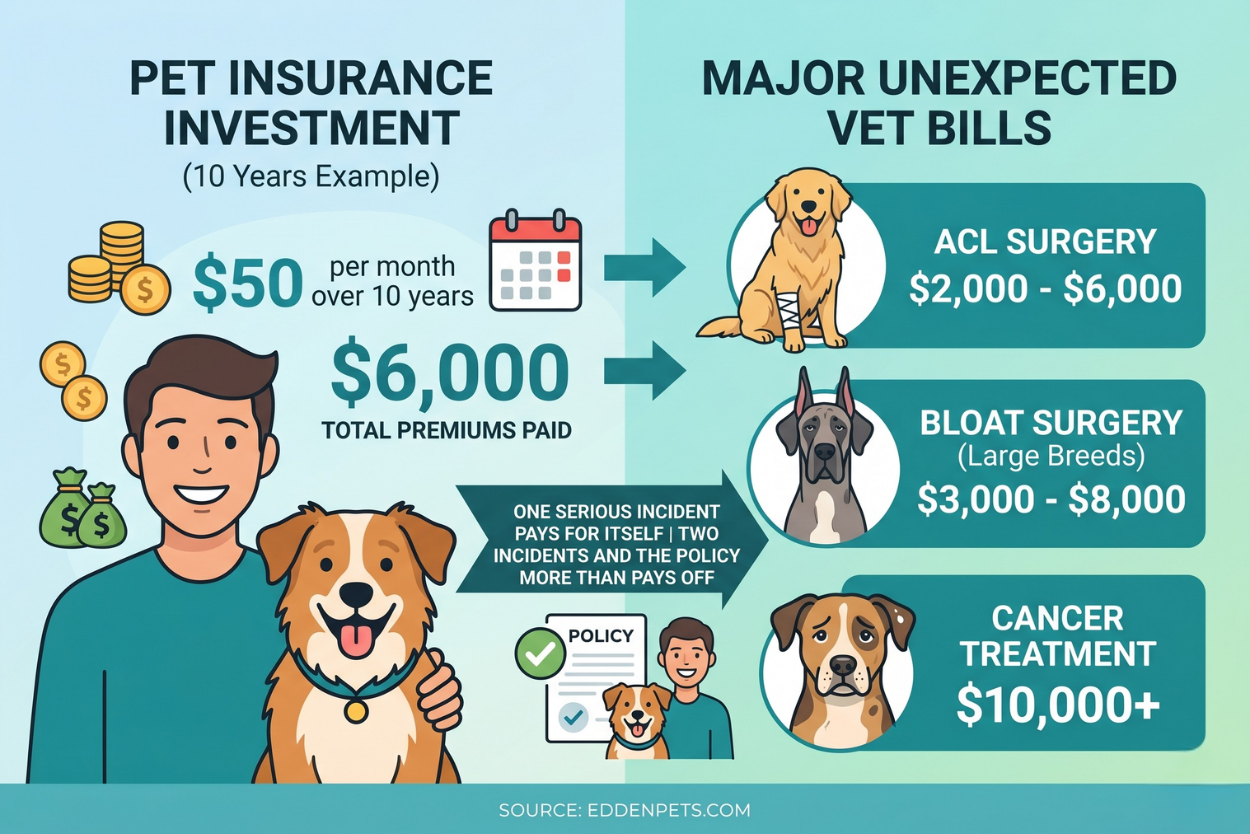

Here’s one way to think about it. If you pay $50 per month for dog insurance over 10 years, you’ll spend $6,000 in premiums. A single ACL surgery costs $2,000–$6,000. Bloat surgery in a large breed runs $3,000–$8,000. Cancer treatment can easily exceed $10,000. One serious incident, and the policy has more than paid for itself. Two incidents, and it’s not even close.

On the flip side, some pets go their entire lives without a major health event. If you’ve got a healthy mixed-breed cat in a low-cost state, your premiums might outpace your claims over a lifetime. In that scenario, setting aside the equivalent premium in a savings account — essentially self-insuring — can be a rational strategy.

But here’s the part the spreadsheet doesn’t capture. Insurance changes the conversation you have at the vet’s office. Without coverage, a $5,000 treatment recommendation becomes a gut-wrenching financial decision. With coverage, it becomes a medical decision.

That shift matters more than most people anticipate until they’re living it. According to the AVMA, pet owners who carry insurance are more likely to pursue recommended treatments and seek care earlier.

Breed-Specific Pricing: What You’ll Actually Pay

State averages are a starting point, but nobody insures an “average” pet. Your actual premium depends on your specific animal, and breed is one of the biggest variables.

The most expensive dog breeds to insure tend to be those with well-documented hereditary health risks. Rottweilers, Great Danes, Bernese Mountain Dogs, English Bulldogs, and French Bulldogs consistently sit at the top of the pricing scale. A French Bulldog in a high-cost state can easily run $80–$90 per month for accident-and-illness coverage.

Mixed-breed dogs, on the other hand, generally benefit from greater genetic diversity and lower incidence of breed-specific conditions. That translates into premiums that are often 30–50% lower than their purebred counterparts. It’s one of the few areas in pet ownership where the “mutt advantage” shows up in dollars.

Cats are almost always cheaper to insure than dogs. Monthly premiums for cats range from about $19 in the cheapest states (Wyoming, Mississippi) to $32 in the most expensive (Arizona, California). Breed variation exists for cats too — Sphynx, Himalayans, and Maine Coons tend to carry higher premiums — but the spread is narrower than it is for dogs.

If you’re curious what your specific pet would cost, the best move is to pull quotes from at least three or four insurers. Pricing varies more between companies than many people realize. Insurify, for instance, aggregates quotes from 10+ partner companies, and the cheapest and most expensive options for the same pet can differ by 40% or more.

How to Lower Your Pet Insurance Premium

You don’t have to accept the first price you see. There are several straightforward ways to bring your monthly cost down without gutting your coverage.

1. Enroll when your pet is young

This is the most impactful move you can make. Premiums are lowest for puppies and kittens, and — critically — pre-existing conditions won’t be excluded if you sign up before they develop. A condition that shows up after enrollment is covered. The same condition diagnosed before enrollment? Excluded for the life of the policy. Timing matters.

2. Raise your deductible

If you can comfortably absorb a $500 vet bill out of pocket, choosing a $500 deductible over a $250 one will reduce your monthly premium meaningfully. You’re essentially telling the insurer you’ll handle the small stuff yourself. They reward that with a lower rate.

3. Consider an accident-only plan if you want bare-bones protection

These plans cover injuries — broken bones, lacerations, foreign-body ingestion — but not illnesses. They typically cost $10–$20 per month and function as a financial safety net for worst-case physical emergencies. They won’t cover cancer or chronic conditions, but for budget-conscious pet owners, they keep the catastrophic-cost scenario off the table.

4. Look for multi-pet discounts

Most major insurers knock 5–10% off your premium for each additional pet on your account. If you’ve got two dogs or a dog and a cat, that adds up quickly.

5. Ask about affiliation discounts

Some insurers partner with employers, alumni associations, military organizations, and groups like USAA to offer reduced rates. It’s worth a quick check before you commit.

6. Shop around for options

This sounds obvious, but most people get one quote and stop. Pet insurance is one of the few insurance categories where prices can vary dramatically between companies for the same animal. Three to four quotes is the minimum. Five is better.

The Bigger Picture: Where This Market Is Headed

The U.S. pet insurance market is growing fast — over 20% annually for the past several years — but it’s still tiny compared to where it could go. Only about 6.4 million pets in the U.S. were insured at the end of 2024, out of a total pet population north of 163 million. That’s a penetration rate of just 3.9%.

To put that in perspective: Sweden has had pet insurance since 1924. Nearly a century of cultural normalization means that insuring your dog there is treated the same way Americans treat car insurance — you just do it. The U.K.’s 25% penetration rate tells a similar, if less extreme, story. The U.S., by contrast, only started seeing meaningful consumer adoption in the last five to seven years.

What’s pushing adoption now? A few things.

Vet costs are rising faster than general inflation, which makes the financial case for coverage more compelling. Embedded insurance — where coverage is offered at the point of pet adoption or purchase — is making enrollment easier and more automatic.

And millennials, who now make up the largest share of pet owners, tend to view pets more like family members and treat pet insurance as a natural extension of responsible care.

State-level legislation is evolving too. More states are introducing pet insurance-specific regulations that require standardized disclosures about what policies cover, how premiums are calculated, and what constitutes a pre-existing condition. That kind of transparency should make the market more competitive over time, which is generally good news for consumers.

So, Is It Worth It in Your State?

There isn’t a single right answer, because the calculation depends on your specific animal, your financial situation, and your tolerance for risk. But here’s a framework that works.

If you have a purebred dog — especially a breed with known health vulnerabilities — in a state with average or above-average vet costs, pet insurance is almost certainly a smart financial decision. The odds of a major claim are high enough, and the potential bills large enough, that the premium pays for itself in expected value alone.

If you have a healthy mixed-breed cat in a low-cost state and you’re disciplined enough to set aside $30 per month in a dedicated savings account, self-insuring is a defensible choice.

For everyone in between — which is most people — it comes down to whether you want to turn an unpredictable, potentially crushing expense into a predictable monthly line item. That peace of mind has a value that doesn’t show up on a balance sheet, but it’s real.

Whatever you decide, don’t wait until your pet swallows a sock🧦 to figure it out.